We must zoom out and revisit first principles. How did we get here? We'll gain a broader understanding of how to effectively apply the 4% rule (or another withdrawal rate) to our retirement scenario.

Before the article, check out the latest on my podcast, Personal Finance for Long-Term Investors:

- On Apple Podcasts

- On Spotify

- On YouTube

Now, here’s today’s article:

Reader Brent wrote in last week:

I probably need to read Bill Bengen’s book but I have a question about the 4% (or now 4.7%) Withdrawal Rule.

Seems to be that a pretty conservative investment could get you a Return Rate of 4% (or even 4.7%) so is it correct in thinking that you are really only digging into the principal of your retirement savings for inflation?

With that thought in mind maybe throwing a high % retirement savings in Laddered TIPS is the way to go since it accounts for inflation.

Or have I got this all wrong?

Brent – that’s a terrific and prevalent question. Retirees often hear “the 4% rule” and think, “Hmm – so, I just need to find an investment that returns 4% per year, and then I’m set for all my retirement?”

I believe that most retirees (and plenty of financial professionals) do not understand the process, the data, the assumptions, or the results of “the 4% rule.”

- It’s built on assumptions.

- Those assumptions are understandable, but rarely applicable to our individual, unique lives.

- The data behind the study is “the best we can muster,” but still limited.

- All these assumptions above provide not just one outcome, but a spectrum of outcomes.

- Then, we take those outcomes and build a singular rule that skews ALL THE WAY to the conservative side of that spectrum.

That is the 4% rule. Despite its apparent limitations and flaws described above, the 4% Rule casts a huge shadow over the world of retirement.

We must zoom out and revisit first principles. How did we get here? We’ll gain a broader understanding of how to effectively apply the 4% rule (or another withdrawal rate) to our retirement scenario.

Forget What You Know

Epictetus once wrote,

“It is impossible for a man to learn what he thinks he already knows.”

So I want to ask you, at least for the sake of this article: please set aside what you know about the 4% rule. I want you to pretend you know nothing.

We are going to build a “rule” from the ground up.

What’s The Big Problem?

The problem at the genesis of today’s article is familiar to many retirees:

How much can I safely spend from my investments in retirement without running out of money?

It’s a simple question, but the devil is in the details. The issue is that there are too many variables built into that simple sentence for us to solve all of them simultaneously.

- What exactly does “safely spend” mean?

- Will your spending change from year to year?

- How is your portfolio allocated among different assets?

- How long will your retirement last?

- What does inflation look like during this retirement period?

- And, of course, what will investment returns look like during your retirement?

Our answers to these questions ultimately determine the outcome of our analysis. That’s really important! So I’ll repeat it: our answers to these questions ultimately determine the outcome. If we make poor assumptions, our outcome becomes flawed. Garbage in, garbage out.

Let’s Make Some (Good) Assumptions…

The retirement analysis community…including the original Trinity Study scholars, Bill Bengen (father of the 4% rule), Wade Pfau (who has updated the 4% rule a few times), and more…seem to all agree on a few assumptions:

Safe Spending

“Safe spending” means ending retirement (a.k.a. dying) with $1 or more in our portfolio. If the final number is zero or negative, you did not safely spend.

I get it. That makes sense.

Except…ending retirement with $1 doesn’t feel particularly safe. It feels like we cut it too close.

Then again, ending retirement with 300% of the assets you started retirement with…that feels too safe.

The problem is that it’s impossible to define “safe spending” for all retirees in all scenarios. The best we can muster is “die with at least $1.” That’s fine. I’m not suggesting we drastically alter that assumption. But I am suggesting we place an asterisk here.

*I get it, but I don’t like it, and don’t think most real people want to think this way.

Quick sidenote…My free weekly newsletter helps busy professionals and retirees avoid costly mistakes and grow lasting wealth to and through retirement. Join 3900+ subscribers, for free.

Constant Spending

Does spending change in retirement? Of course! Our retirement spending differs from our working years and continues to change from year to year.

But there’s a problem. Your retirement spending looks different than my retirement spending, and we both look different than everyone else out there.

How do we solve this problem?

Simple. We assume everyone has constant retirement spending. Instead of everyone having a unique spending profile, we assume that nobody’s spending ever changes.

Hmmm…that doesn’t really feel like a solution.

You’re right. It’s a one-size-fits-all assumption that, in reality, fits nobody. But the problem with “rules of thumb” is that we simply cannot make them “fit all.”

When we do actual retirement analysis for a unique family situation, understanding that family’s unique spending and other cashflows is a must. However, to create a broad rule, we must make concessions. Once again, an asterisk.

*I get it, but I don’t like it, and don’t think most real people want to think this way.

How is Your Portfolio Allocated?

Again, to each their own.

I like to approach this question from a “goals-based” lens. Your financial goals inform your timelines. Timelines inform appropriate risk. That risk informs asset allocation. We start with goals, we end with an asset allocation.

Most retirees I’ve worked with tend to have “risk on” allocations (stocks, real estate, alternatives) ranging from ~40% to 75% of their portfolio, with the remainder in “risk off” assets.

How Long Will My Retirement Last?

Time for one of the best one-liners in financial planning:

Tell me when you’re going to die, and I’ll build you a perfect financial plan.

This brings up one of the broader challenges in financial planning. Should we build plans for the average person and for average circumstances? Or should we account for exceptional people and exceptional circumstances?

Will you be the 1-in-30 retiree who lives to age 100? Or would you rather plan for an “average” retiree life expectancy of low-to-mid 80s?

This is a tricky question. For general rules of thumb, the retirement planning community says, “Eh…how about 30 years?“ While that feels reasonable, it ends up specifically applying to about ~4% of retirees. Then again…without a crystal ball, we can’t know what our exact retirement timeline will look like.

Inflation? Investment Returns?

What should we assume for investment returns and inflation’s bite? My crystal ball is broken. Perhaps yours is working?

Here’s another funny truth about financial planning. We make sure to remind ourselves and everyone else that “past performance is not predictive of future results.” We’ve all heard it. Fewer of us, I’d argue, truly take it to heart. But we should take it to heart. It’s important.

But, despite hearing that phrase on thousands of golf tournament TV ads, the entire world of financial planning then turns around and says,

“Let’s build a towering monument of retirement analysis on a foundation of…past performance, and only past performance.”

Whether we’re looking at inflation or investment returns, any retirement planning tool you’ve ever used is built on a database of historical market returns.

I get it. I’m not sure what the better alternative is.

I just think it’s crucial we realize what we’re doing – and what we’re not doing. This isn’t some infallible science. We’re not dealing with laws of physics.

Instead, all we’re doing is building a specific scenario and determining how successful that scenario might have been in the past.

But Jesse! What About Monte Carlo Analysis?!?!

Some of you uber-nerds might push back here, thinking that Monte Carlo analyses don’t actually use historical returns, but instead create new sequences of possible market returns never seen before.

This is a half-truth. If you’re not careful, you’ll fall into the classic analyst’s trap of “garbage in, garbage out.” I can speak somewhat intelligently here because we used to use Monte Carlo analyses as part of designing and analyzing orbital satellites. Monte Carlo outputs are only as worthwhile as the input you give them.

Financial planning Monte Carlo analyses generally work in one of three possible ways.

- Historical resampling: Shuffling actual historical returns (e.g., S&P 500 and bond returns) into new sequences.

- Statistical sampling: Assuming that investment returns follow a particular probability distribution (often normal or log-normal) based on historical averages, standard deviations, and correlations. Then, create new datasets using that historical probability distribution.

- Hybrid approaches: Some programs combine historical data with Monte Carlo randomization to smooth out anomalies.

Ultimately, all of these approaches are based on historical data. That’s plain and simple.

If a Monte Carlo analysis generates investment return data without basing it on historical precedent, then it’s essentially making up data out of thin air.

Do We Have Answers Yet?

Man alive! That’s a lot of preamble, Jesse!!!

I’m sorry, I’m sorry. But it’s essential! Once we make our assumptions, we can then take our hypothetical retirement and run it through our historical scenarios.

Once we know our safe spending, our investment allocation, our retirement length, and our inflation-adjusted returns, THEN we can ask,

“How often over the past ~100 years would my retirement have actually worked? How often would it have failed?”

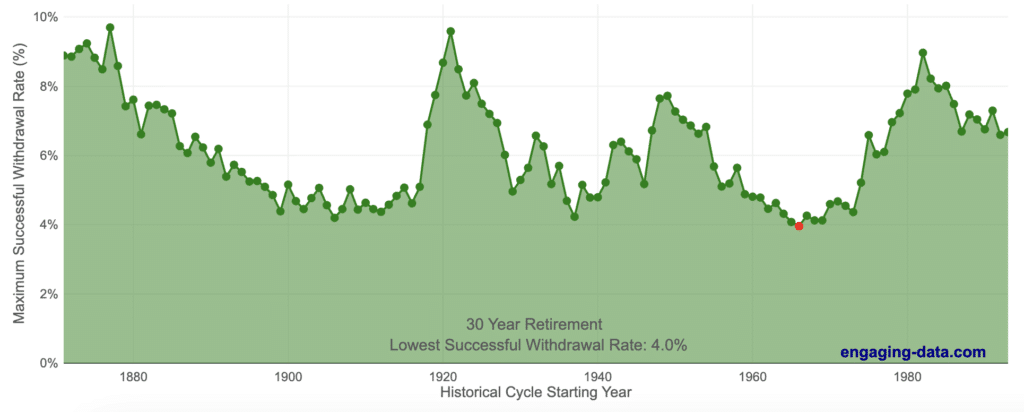

For example, let’s look at the actual 4% rule assumptions:

- To run out of money = failure.

- Our spending will never change, save for inflation adjustments.

- Our portfolio is allocated 50% to stocks (all US stocks) and 50% to bonds (high-grade Treasury bonds)

- Our retirement will last 30 years.

- Inflation and investment returns will be based solely on historical data.

What results do we see?

- In over 50% of historical scenarios, we could have actually withdrawn more than 6% per year and been totally safe.

- In fact…in some scenarios, we could have withdrawn more than 8% per year and still been safe.

- But in the worst scenario (which you can see with a red dot, above), we could only withdraw 3.9% per year to avoid depleting our funds.

This. This right here. This is the precise genesis of the 4% rule.

We start with a list of dubious assumptions. Then we take the very worst of the outcomes created by those assumptions. And then we say, “Let’s make sure THAT is where we set the bar.”

I do not like that. I don’t think you should like that either.

Brent’s Question – Do TIPS Help?

Back to Brent’s question…does Treasury inflation-protected securities (TIPS) help here? Can a TIPS ladder essentially zero-out the inflation concern, provide a guaranteed return to negate the market risk, and thus “guarantee” we can live off more than 4%?

I totally understand the question, Brent. But I hope I’ve convinced all of you why that question (or many other similar questions asked by many other DIYers) are simply the wrong questions to ask.

I hope my explanation above shows that the 4% Rule is already flawed. It’s based on unrealistic assumptions. The resulting “4%” – the namesake itself! – is overly conservative. It’s nothing more than a rough rule-of-thumb for financial planning nerds to use on their back-of-the-napkin math.

I mean that. Use the 4% rule in casual conversations to establish a conservative baseline. Then you must do the real work for your specific circumstances.

The 4% Rule is not a guidepost or a milestone. We should not compare any asset (TIPS or otherwise) against a 4% return to determine its merit or lack thereof.

Is There A Better Way?

One of the problems here is that there’s so much “luck of the draw.”

Someone who retired in the early 1980s could have lived an entire 30+ year retirement withdrawing 8%+ per year, adjusting each year for inflation. They could have retired with “only” 12x their annual spending saved in their portfolio.

But someone in the same circumstances retiring in the mid-1960s could only have withdrawn 3.9% per year, and would have needed 25x their annual spending to retire.

That’s a massive difference, solely due to their good or bad luck in timing.

Here’s my personal solution:

- Using the true 4% Rule is only a starting point.

- The 4% Rule creates a “conservative bookend” based on one-size-fits-all criteria.

- If you want an easy (albeit still flawed) rule-of-thumb to be more optimistic, it’s this:

- A 5% withdrawal rate has been safe in most historical scenarios.

- A 6% withdrawal rate has been safe for about half of the historical scenarios.

- Your specifics matter a lot here.

- If you’re willing to be flexible – specifically, by decreasing your spending during poor market periods – then you’ll surely avoid many of the adverse outcomes that come from higher withdrawal rates.

- Ultimately, if you want precision, your unique retirement attributes are a MUST to home in on a better answer for you.

You must answer these questions for yourself…

- What exactly does “safely spend” mean?

- Will your spending change from year to year?

- How is your portfolio allocated among different assets?

- How long will your retirement last?

- What does inflation look like during this retirement period?

- And, of course, what will investment returns look like during your retirement?

And even then, take your result with a grain of salt. I know that’s a tough pill to swallow, and not nearly as comfortable as the easy math of the 4% rule. So let me throw it back to Epictetus again:

“Make the best use of what is in your power, and take the rest as it happens.”

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!