Most retirees budget for Medicare premiums. What they don’t budget for is paying 2–3x more than their neighbor for the exact same coverage. That’s what IRMAA does. If your income crosses certain thresholds, Medicare adds a surcharge to your Part B and Part D premiums—sometimes totaling $10,000+ per year for a married couple. The worst […] The post How Retirees Can Manage Income to Avoid Higher 2026 Medicare Premiums (Your IRMAA Playbook) appeared first on Define Financial.

Most retirees budget for Medicare premiums.

What they don’t budget for is paying 2–3x more than their neighbor for the exact same coverage.

That’s what IRMAA does. If your income crosses certain thresholds, Medicare adds a surcharge to your Part B and Part D premiums—sometimes totaling $10,000+ per year for a married couple.

The worst part? The income that triggers IRMAA was earned two years ago. By the time you get the notice, it’s too late to change it.

In this guide, I’ll break down:

- Exactly what IRMAA is and how Medicare calculates it

- The 2026 income thresholds that trigger surcharges

- Proven strategies to reduce or avoid IRMAA without disrupting your retirement plan

Let’s get into it.

Key Takeaways

- IRMAA surcharges link Medicare premiums to your modified adjusted gross income (MAGI). Even modest increases can move you into a higher bracket, raising costs for both Part B and Part D.

- You can reduce IRMAA exposure through careful income planning. Strategies include staggering Roth conversions, balancing withdrawals across account types, using HSAs or Roth IRAs, and timing large gains or distributions.

- Certain life events allow you to appeal your IRMAA surcharges. Retirement, divorce, or the death of a spouse may qualify you to file Form SSA-44 so premiums reflect your current income rather than older tax data.

What Is IRMAA and How Does It Work?

IRMAA stands for Income-Related Monthly Adjustment Amount. It’s a surcharge Medicare adds to your Part B and Part D premiums if your income exceeds certain thresholds.

It’s not a penalty—it’s a pricing structure that ties higher incomes to higher premiums. And it doesn’t apply to everyone. If your income stays below the first threshold, you’ll pay standard premiums and nothing more.

Which parts of Medicare does IRMAA affect?

IRMAA applies to two parts of Medicare:

- Part B — Medicare’s medical insurance (outpatient care, doctor visits, lab work)

- Part D — Prescription drug plan (optional, but important)

If you’re subject to IRMAA, you’ll pay the base plan premium plus an income-based surcharge in your monthly premiums. Social Security calculates the amount and often deducts it automatically from monthly Social Security payments.

How Medicare calculates your IRMAA

Medicare calculates IRMAA using your modified adjusted gross income (MAGI), which begins with your adjusted gross income (AGI) and adds back certain items—most notably, tax-exempt interest income from municipal bonds.

Here’s the catch: Social Security uses income data from the tax return filed with the Internal Revenue Service two years prior. So your 2026 IRMAA is based on your 2024 tax year MAGI. Simply put, the higher your MAGI, the larger your Medicare surcharges or premiums can be. By the time you receive the surcharge notice, the income that triggered it is already in the past.

How IRMAA brackets work

IRMAA is divided into income brackets, and each bracket boundary is an IRMAA threshold; once your income crosses one, your surcharge jumps to the next level—sometimes by a meaningful amount.

As a result, even a small increase in income level near one of these thresholds can have an outsized impact.

Go just $1 over a bracket boundary, and you owe the full surcharge for that higher tier, not a prorated amount.

Stay just below it, and you avoid paying IRMAA surcharges at the higher tier altogether.

Why Retirees Need to Pay Attention to IRMAA

Retirement requires paying attention to Medicare surcharges as part of broader financial planning, and IRMAA surcharges add up faster than most retirees expect.

A single person in the highest bracket could pay over $6,000 per year in surcharges alone.

For married couples, that figure can double if they file a joint tax return or are married filing jointly, since IRMAA applies to each spouse individually.

That’s real money that could go toward travel, family, or simply staying flexible instead of covering this additional cost.

Routine retirement moves can trigger IRMAA

The tricky part is that many normal financial decisions can push your income over a threshold without warning:

- Taking a large withdrawal from a Traditional IRA or 401(k)

- Selling real estate or exercising stock options

- Realizing capital gains from a portfolio rebalance in a brokerage account

- Completing a Roth conversion

Each of these may be the right move for your situation. But the timing of that move determines whether you’ll pay standard premiums or thousands more.

Why IRMAA belongs in your income plan

Most retirees plan for taxes. Fewer build IRMAA into their retirement income plan, even though it functions like an extra tax on higher incomes.

Building IRMAA awareness into your withdrawal strategy helps you make cleaner tradeoffs.

You can still take the gains, do the conversion, or sell the property, but your investment strategy should account for those moves in a year when the surcharge impact is minimized, or avoided entirely.

The goal isn’t to dodge every bracket at all costs. It’s to stop leaving money on the table by ignoring a surcharge that can cause you to pay higher premiums.

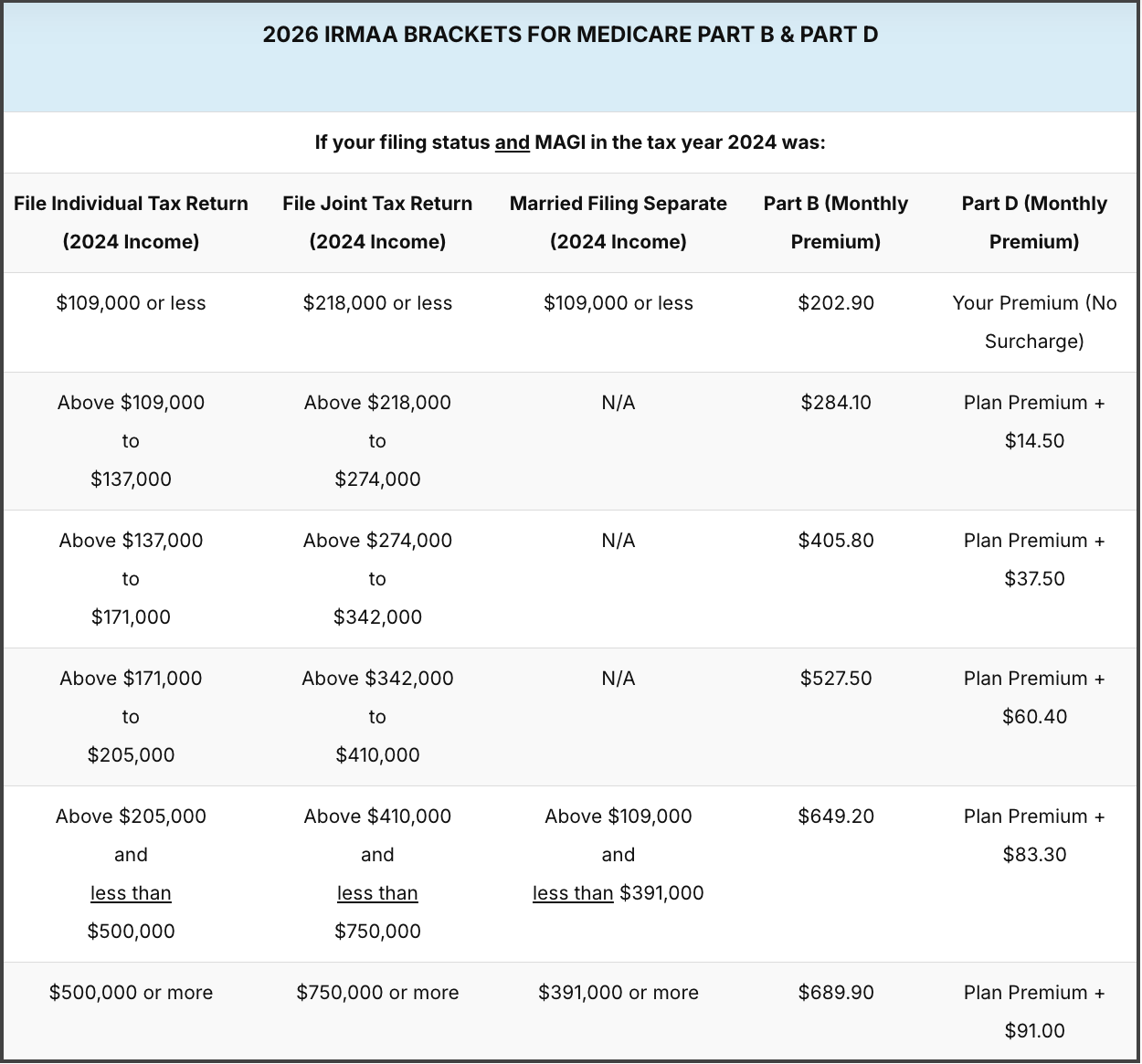

2026 IRMAA Surcharges at a Glance

If your 2024 tax return pushed your Modified Adjusted Gross Income (MAGI) above certain levels, your 2026 Medicare premiums may include extra charges.

Here’s what you need to know for quick reference:

- Base Medicare Part B monthly premiums (2026): $202.90 per month

- Average Medicare Part D monthly premiums (2026): $38.99 per month

These amounts affect the total cost of coverage, not just the surcharge portion.

2026 IRMAA Brackets (Based on 2024 MAGI):

- Single filers ≤ $109,000 / Joint filers ≤ $218,000: No IRMAA surcharges

- $109,001–$137,000 (single) / $218,001–$274,000 (joint): Part B +$81.20, Part D +$14.50

- $137,001–$171,000 (single) / $274,001–$342,000 (joint): Part B +$202.90, Part D +$37.50

- $171,001–$205,000 (single) / $342,001–$410,000 (joint): Part B +$324.60, Part D +$60.40

- $205,001–$499,999 (single) / $410,001–$749,999 (joint): Part B +$446.30, Part D +$83.30

- $500,000 or more (single) / $750,000 or more (joint): Part B +$487.00, Part D +$91.00

If You’re Married Filing Separately in 2026:

- Above $109,000 and less than $391,000: Part B +$649.20, Part D +$83.30

- $391,000 or more: Part B +$689.90, Part D +$91.00

Key Strategies to Avoid or Reduce IRMAA Surcharges

You can’t opt out of IRMAA, but you can often influence the income that triggers it.

The focus is making thoughtful, coordinated decisions that account for both taxes and healthcare costs.

In some cases, that may mean accepting a surcharge if it leads to a better overall outcome, especially around timing points like beginning Medicare.

Whether you choose traditional coverage or Medicare Advantage, IRMAA still affects Part B and Part D costs, so the goal is to manage surcharges while keeping your broader Medicare plan intact.

Here are several proven strategies to help manage IRMAA:

Manage taxable income carefully: Blend withdrawals across traditional IRAs, Roth accounts, and taxable accounts so no one source pushes you past a threshold. Place interest-heavy holdings in tax-deferred accounts where they fit your mix.

Spread out Roth conversions: Converting in smaller, scheduled amounts can build future tax-free income while moderating current MAGI. Annual guardrails based on your tax bracket and IRMAA tiers help you avoid surprise jumps.

Leverage tax-advantaged accounts: Roth IRAs and health savings accounts (HSAs) add flexibility because qualified Roth withdrawals and HSA payments for medical bills do not increase MAGI. Pre-Medicare households can also build HSA balances during working years to spend tax-free later.

Control timing of income events: Plan big moves, such as selling appreciated positions, exercising options, or taking distributions, during years when other income is lighter. Staggering sales or splitting withdrawals across tax years can keep you below a higher tier.

Consider charitable giving strategies: Qualified Charitable Distributions (QCDs) from IRAs send dollars directly to charity and exclude the amount from taxable income, which also reduces Modified Adjusted Gross Income (MAGI). Wile donor-advised fund contributions will reduce your taxable income, they will not reduce your MAGI for IRMAA purposes.

Pay attention to Social Security timing: Delaying benefits can lower MAGI in early retirement and create room for conversions or gains. Coordinating start dates with your withdrawal plan makes the most of low-income windows before required minimum distributions (RMDs) begin.

Special Situations Where You May Avoid IRMAA

Some life changes can reduce income quickly, which means last year’s tax return may no longer reflect your situation. When that happens, an IRMAA decision based on old data can be higher than it should be.

Social Security allows an appeal when you experience a qualifying life-changing event, such as retirement, divorce, the death of a spouse, or a significant loss of income from a work reduction.

You can ask the agency to use more recent information and recalculate your adjustment by filing Form SSA-44 with the Social Security Administration.

This form lets you report your updated circumstances, estimate your MAGI for the relevant period, and provide supporting documentation. Depending on your situation, you may be able to file online or submit the request through your local Social Security office.

If approved, your IRMMA surcharges will be reduced to reflect your current income rather than the prior tax return, which can avoid IRMAA tax for two years.

Practical Examples of IRMAA Triggers

IRMAA charges often stem from reasonable financial moves. The challenge is that timing matters. Even one decision can raise MAGI enough to cross a surcharge threshold. Recognizing these frequent triggers can guide you in choosing whether to spread out, divide, or postpone an action:

Selling real estate or a business: A major sale can create a one-time spike in taxable income. Adjusting the closing date or considering installment-sale treatment can soften the impact.

Taking large IRA or 401(k) withdrawals: Using a lump sum for a remodel, debt payoff, or a large gift may push you into a higher tier. Splitting withdrawals across two calendar years often helps contain MAGI, though it can still affect your federal income tax bill.

Realizing capital gains from investments: Trimming a concentrated stock position or rebalancing a portfolio can increase taxable income. Pairing capital gains with losses through tax-loss harvesting in a taxable account, or waiting until a lower-income year to realize gains, can help reduce tax exposure.

Completing full Roth conversions in one year: Converting everything at once builds long-term tax-free income but may create short-term surcharges and a larger current-year tax cost. A multiyear conversion plan typically provides a better balance.

Starting pensions or annuity payouts: New guaranteed income streams add to MAGI, reducing flexibility for Roth conversions or other planning moves. Coordinating start dates with your withdrawal strategy keeps options open.

IRMMA FAQs

Does everyone pay IRMAA?

No. IRMAA only applies if your modified adjusted gross income (MAGI) rises above certain thresholds. Many retirees will never pay it if their income stays below those levels.

Can IRMAA surcharges go away once applied?

Yes, they can. IRMAA isn’t permanent. If your income later drops below a threshold, your surcharge will fall back down as well. Moreover, if a drop in income is due to a qualifying life change (like retiring, getting married, divorcing, or losing a spouse), you may ask for an earlier review.

How often are IRMAA brackets updated?

IRMAA brackets are reviewed annually. Each fall, the Social Security Administration publishes the following year’s Medicare premiums and surcharge brackets. These brackets are indexed to inflation, so they can change even if your income stays the same.

Is IRMAA the same as paying higher Medicare premiums in general?

Not exactly. Standard Medicare Part B and Part D premiums apply to everyone who is enrolled. IRMAA is a separate, income-based charge that’s added on top of those base premiums. Your base premium remains the same, but once your income crosses a threshold, you’ll pay an additional monthly surcharge for both Part B and/or Part D.

Can delaying Social Security help with IRMAA?

Yes, in certain situations. By delaying Social Security benefits, you may be able to reduce taxable income in the early years of retirement, giving you more room to manage other income sources like Roth conversions or capital gains.

This window, between when you retire and when you eventually claim Social Security, can often be used strategically to keep MAGI below IRMAA thresholds. However, once you do start benefits, those payments count toward MAGI, so it’s important to coordinate the timing with your overall retirement withdrawal strategy.

How We Can Help You Avoid IRMAA Surcharges

Coordinating Medicare costs with taxes and portfolio withdrawals helps your plan work the way you expect. That starts with mapping out income sources year by year and seeing where IRMAA tiers line up with your goals.

At Define Financial, we build a multiyear retirement income plan that helps you see how different decisions may affect your taxable income, Medicare premiums, and long-term tax bill. That includes identifying lower-income years, evaluating partial Roth conversions, planning large transactions carefully, and helping you avoid preventable surprises.

If you want help navigating Medicare premiums, managing IRMAA surcharges, and building a more coordinated retirement income strategy, schedule a free Retirement Strategy Session.

The post How Retirees Can Manage Income to Avoid Higher 2026 Medicare Premiums (Your IRMAA Playbook) appeared first on Define Financial.