Central banks just sent their clearest signal yet that gold purchases are far from over. According to a recent survey, nearly half of governments plan to add more physical gold to their stockpiles over the next 12 months — the highest level of commitment ever recorded. At the same time, nearly three-fourths of monetary authorities... Read more »

Central banks just sent their clearest signal yet that gold purchases are far from over. According to a recent survey, nearly half of governments plan to add more physical gold to their stockpiles over the next 12 months — the highest level of commitment ever recorded.

Central banks just sent their clearest signal yet that gold purchases are far from over. According to a recent survey, nearly half of governments plan to add more physical gold to their stockpiles over the next 12 months — the highest level of commitment ever recorded.

At the same time, nearly three-fourths of monetary authorities expect the dollar’s share of global reserves to decline over the next five years. As one of the most influential drivers of the gold market, the expanding central bank gold appetite is a compelling signal of the metal’s future growth.

Nearly Half of Reserves Plan to Increase Stockpiles

Every year, the World Gold Council — a leading voice in the industry — conducts a Central Bank Gold Reserves Survey to take the pulse of reserve officials’ precious metals strategy. The 2026 results reveal a stark shift in the global economic landscape as central banks validate their intentions to continue loading up on gold while shedding the USD.

A staggering 45% of respondents anticipate their gold reserves to increase over the next year, which is the most bullish reading observed since the survey began in 2018. For context, this figure stood at 18% when the analysis was first launched.

In sharp contrast to the nearly half of gold-hungry respondents, only 1% of reserve managers actively plan to offload some of their assets. Beyond a bland statement of confidence, these results reflect real-world policy decisions of the world’s largest and most influential gold purchasers.

Central Banks Continue Buying at Historic Levels

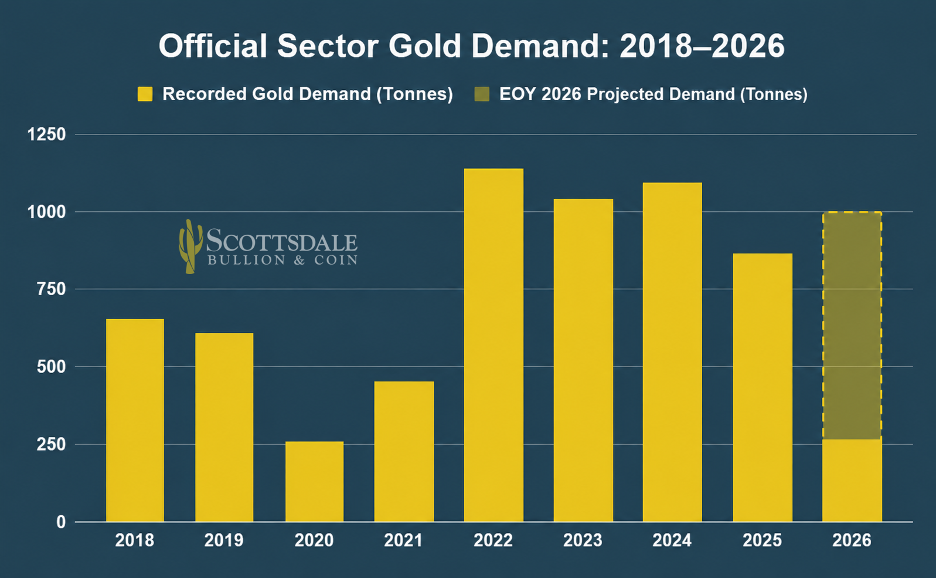

What’s more, this comes as central banks have purchased more than 1,000 tonnes of gold annually, on average, for four consecutive years. Following years of moderate consumption, official buyers accelerated their consumption in 2022 and have only shown signs of speeding up.

Between 2022 and 2024, annual figures leapt over 1,000 tonnes, and then hit 863 tonnes in 2025. Between January and April of 2026, purchases have reached 260 tonnes, and UBS commodity analyst Giovanni Staunovo anticipates a year-end total of 750 to 1,000 tonnes, according to CNBC.

Gold’s Strategic Role Continues to Expand

On top of a rising tide of gold buying over the next year, reserve officials see yellow metal taking an increasingly centralized role in the global financial system. Revealingly, 89% of central banks believe physical gold reserves will augment in the subsequent 12 months.

Furthermore, 84% of central bank managers anticipate the metal will account for a larger share of total reserves within five years. For context, 76% of respondents affirmed that sentiment last year, underscoring growing confidence in gold’s long-term role as a reserve asset.

Crucially, gold’s ascent within the global reserve framework isn’t only a matter of projection. Last year, the worldwide banking system reclassified gold as a Tier 1 asset, placing it on par with fiat currencies and U.S. Treasuries. More recently, gold overtook the USD and euro as a share of global reserves in terms of raw value.

Confidence in the Dollar Is Slipping

As gold continues to gain prominence within global reserve portfolios and the broader economic system, the USD is losing grip on its status as world reserve currency. In the WGC survey, 74% of central banks anticipate the dollar’s share of global reserves to decline over the next five years.

Although a distrust of fiat currencies is certainly at play, the greenback is in a uniquely vulnerable position as a de-dollarization trend picks up steam. Mirroring this concern, reserve managers believe that the euro and Chinese renminbi will maintain their current share of reserves over the next half decade.

Why Central Banks Continue Favoring Gold

The survey also asked reserve managers why they hold gold. More than three-quarters of respondents identified the following factors as relevant to their decision-making:

- Performance During Times of Crisis (90%) — Gold has historically preserved value during periods of financial and geopolitical turmoil.

- Long-Term Store of Value/Inflation Hedge (84%) — The metal helps protect purchasing power against currency debasement by keeping pace with inflation.

- Portfolio Diversification (83%) — Physical gold often behaves differently than traditional reserve assets such as bonds and currencies.

- Geopolitical Risk Hedge (81%) — Gold can offer protection against geopolitical instability and global uncertainty.

- No Default Risk (80%) — Unlike sovereign debt or other financial assets, physical gold carries no counterparty risk.

- Reserve Diversification Policy (79%) — The yellow metal supports broader efforts to reduce concentration in any single reserve asset.

- Historical Gold Holdings (76%) — Many central banks continue to view gold as a core strategic reserve asset due to longstanding ownership traditions.