If we think that the stock market is overvalued right now, doesn’t it make sense to sell some stocks and move that money to cash?

Before the article, check out the latest on my podcast, Personal Finance for Long-Term Investors:

- On Apple Podcasts

- On Spotify

- On YouTube

Now, here’s today’s article:

Phil wrote in this week:

Jesse – if we do think that the stock market is overvalued right now, doesn’t it make sense to sell some stocks and move that money to cash?

Or is that “timing the market?”

Can’t I just argue it’s smart “rebalancing?”

It kind of feels like semantics!! I’m writing this as a 68-year old retiree (retired since 2017). Interested to hear your thoughts.

I’ve been thinking about this myself, Phil. Yes, valuations are undoubtedly high. But, as Aswath Damodaran might ask, does that mean stocks are overpriced?

And most to the point: should long-term investors and retirees do anything about it?

The “Boglehead” and “Malkiel” in me both know that market timing is a fool’s errand. As John Bogle told us, “Don’t do something; just stand there.”

At the same time…

- Returns have been so good. The S&P 500 return since January 2023 (35 months) is 22.46% per year. These kinds returns do not and cannot continue forever.

- Zooming out, since Phil retired in 2017, the S&P has returned 14.5% per year. Simply outstanding.

- Valuations are high, especially among the biggest stocks in the market.

If there was ever an excuse to time the market, surely this is what it would look like? Or at least, I’m sure that’s the argument Phil and many others are telling themselves.

In fairness to the idea, let’s do this: I’ll share both smart and dumb reasons to shift money into cash right now. Let’s see where your thoughts end up.

Why Move to Cash Right Now

There are logical reasons to consider a move to cash right now.

Risk Reduction and Rebalancing Discipline

Selling some stocks will lock in your gains and protect you if the market does correct sharply. This is purely a risk reduction measure.

If your 60/40 starting portfolio is now closer to 70/30, then I’m all in favor of selling stocks to get back to 60/40…or perhaps 60 / 30 + 10% in cash.

Asset-Liability Matching

If your financial plan includes asset-liability matching or a “goals-based” investing framework, then recent stock market performance might have blessed you with “excess capital.”

The asset-liability framework suggests using low-risk assets (cash, bonds) to cover your spending needs for the near term. Then you use high-risk assets (such as stocks) to cover your long-term spending needs.

But then, you might have all your future liabilities covered, yet still have some money to be deployed. This is excess capital.

It’s money you don’t need. Your financial plan will be successful with or without it. For that reason, you can do what you want with it. Find a great charity. Take a flyer on your nephew’s pizza business. Or, if you’re particularly market-wary right now, keep it in cash.

Cash…Isn’t That Bad Right Now

Overnight /short-term cash interest rates are at ~3.8% as of this writing. That’s not bad!

Cash is a reasonable safety net at the moment, especially for a riskless asset.

Psychological Safety

Cash provides peace of mind during periods of high volatility or uncertainty. Some investors call this a “flight to quality.”

For long-term investors like us, I believe the #1 threat to our portfolios is personal behavior. Great investors’ little secret is temperament.

One of the worst things that can happen is getting burned by a market downturn and swearing off investing forever, convinced investing is simply flawed. We want to avoid “flight or fight” reactions, where we feel the primal urge to sell our stocks simply to survive.

If you need to de-risk to avoid that fate, I’m on board.

Do You Want To Learn More?

If you’re looking for better answers to your money questions,

My free weekly newsletter helps busy professionals and retirees avoid costly mistakes and grow lasting wealth to and through retirement.

Join 4000+ subscribers, 100% free.

Sign up here:

The Bad (or Dumb) Reasons To Move To Cash

I wouldn’t begrudge anyone taking some risk off the table right now. But before you do, it’s important to consider the many reasons to NOT do what you’re thinking.

Market Timing is Notoriously Hard

Predicting the top (and bottom) of the stock market is nearly impossible. Even though some smart people describe the current market as overvalued, the really smart ones also say:

- “Companies’ earnings might catch up to these valuations. There won’t be a “pop” to this bubble. It’ll slowly deflate over a few neutral, mediocre years in the market.” Or…

- “It’ll pop. But we don’t know when. Next month? In 6 months? In 2027? Beyond? We simply don’t know how far these things can go.”

In other words, we don’t know if it’ll pop, and we certainly don’t know when.

That’s why you need to ask yourself some hard questions, like:

- What if you sell your stocks today, and then the market grows for another 24 months? Will you be ok with that?

- Are you going to keep that as cash on hand forever? Or are you planning on buying back into the market eventually?

- What if you buy back in too soon? Meaning…what if you re-buy stock 6 months from now…only to then watch the real crash happen before your eyes?

- What if you buy back in too late? You’ve so convinced yourself that the crash is coming that you sit on the sidelines for years as the market grows away from you.

Are you setting yourself up for harder choices and more regret in the future?

Historical Data – Opportunity Cost and Inflation Erosion

I’m not sure if moving to cash is right or wrong. Only time will tell.

But over the long run, I know that cash historically underperforms stocks, especially after inflation. And if we’re all thinking like long-term investors, we’d best not forget that fact.

Even if current cash interest rates (3.8%) are higher than traditional inflation rates, the simple truth is that cash does not outpace inflation over the long run. By fleeing to cash right now, you are accepting that risk.

You Chose This Portfolio for a Reason.

Back in April 2025, during the “tariff tantrum” and the stock market’s subsequent volatility, I reminded you of that line from Russell Crowe in Gladiator:

“Are you not entertained?! …Is this not why you are here?!”

Similar logic applies right here, right now.

We’ve all shared in amazing returns and now the market might be overvalued, overpriced. Is this not why you are here?!

Part of being a long-term investor is this very trade-off. We receive periods of outstanding returns in exchange for the threat (or reality) of negative performance. This is the bargain we signed up for.

Yet, I do understand the temptation. We’re all “loss averse.”

If we can avoid the negative period…why not?! Can’t we eat our cake and have it, too? That’s a human temptation.

But it’s also changing the terms of our investment pursuit midway through the game. Stay the course.

What’s the Magnitude…and What’s the Benefit?

So you’re committed to this idea of selling your stocks, moving to cash. How are you “right-sizing” your bet?

Let’s do some simple math.

We know a 20%, 30%, 40% drop in the stock market won’t be fun. But…are you going to sell ALL your stocks to avoid that potential drop? Will you just sell off a small portion?

If you’re planning to sell a small sliver of your stocks, what’s the real benefit? For example, selling 5% of your stock portfolio and then *perfectly* timing a 40% market drop just saved your portfolio a whopping 2%.

But then, if you’re planning to sell 50% of your stocks…are you sure? Not only are you violating a key tenet of long-term investing, but you’re doing so with a huge fraction of your net worth?

On the small side, this choice doesn’t move the needle. On the big side, this might ruin your financial future. Where’s your Goldilocks zone?

Why Now?

You need an objective reason why now is the right time for this move. Why not 3 months ago? Why not in 2021?

I’m worried your reason might be,

“Because every media outlet seems to be calling this AI bubble. Surely, where there’s smoke, there’s fire?”

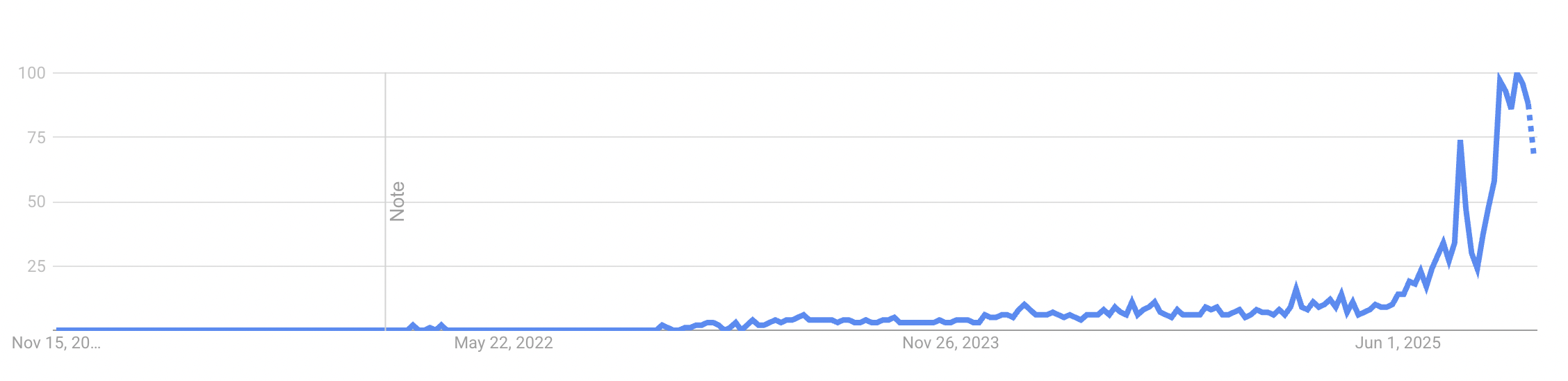

It’s true. Here’s the past 5 years of Google Trend data for the search term, “AI bubble.”

But in response to this idea, I want to invoke some wisdom from Howard Marks’ latest newsletter:

“One of the most prominent characteristics of the financial markets that I’ve detected over the years is their tendency to obsess over a single topic at a given point in time. The topic eventually changes to another, but before it does, it’s often the thing people want to discuss to the near exclusion of everything else.”

Remember Silicon Valley Bank? GameStop? Yield-curve inversion? NFTs? That’s just the last ~4 years!

I know concerns about an AI bubble are everywhere we look. But…are we all in a bit of a financial media “echo chamber?”

I mean, let’s be honest: you’re here reading what’s probably the #219 retirement and financial planning blog on the Internet. You, like me, might be pretty deep in the weeds.

What Should We Do?

To sell, or not to sell?

The way I see it, both choices have rational, numerical, and subjective, emotional components.

On the numerical side, it’s an argument between:

- This thing can’t keep growing forever, vs.

- If you time the market and move to cash, the historical odds aren’t in your favor.

On the emotional side, it’s all about minimizing regret, loss aversion, and avoiding a “fight or flight” scenario.

7 Tips If You’re On the Fence

If you’re still on the fence, here are some tips to help you decide:

- Tie this choice to a timeline. A retiree might say, “I’m going to move one year’s worth of expenses out of stocks and into cash.” You’re measuring this decision in time, not in percentages or dollars. You’re moving long-term runway into the near term.

- Keep this decision small. You don’t need to eat the whole tub of ice cream. Perhaps just one bite will satisfy you? Similarly, can you scratch this current itch in a small yet satisfying way?

- Make this a one-way decision. You’re selling stocks to cash. Fair enough. But do not assume you’ll find the perfect time to move this cash back into stocks. That is a slippery slope. If you need to scratch this itch, don’t let it turn you into a chronic market timer.

- Zoom out. If this seed has been ruminating for years, fair enough. But don’t let 2 months of headlines derail your financial plan.

- Be clear with yourself – are you solving a portfolio problem or a feelings problem? Either can be reasonable; neither is wrong. But be clear about what you’re doing and…

- Write it down. Why are you making this decision? Then, set a reminder to review your rationale it in 6, 12, 24 months.

- Don’t act under urgency. If you think the market is a ticking bomb that could explode any day – I would urge you to pause. You might be letting fear create a sense of urgency, and I doubt we can make sound investing decisions in that mindset.

Phil – thanks for the question and I hope this helps.

These are interesting (but “good”) problems for long-term investors like us.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!