The Best Interest Blog

The Best Interest Blog Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Tune in on:

Now, here’s today’s article:

Reader Jon:Â Jesse, I am not sure why people would buy traditional bonds if you can get a similar yield in an ETF which is more liquid?Â

Lots of other readers:Â my bond funds took a beating in 2022, and some are still underwater. But individual government bonds always return to par! How could you ever want to own a bond fund?

This is a nuanced topic, but since most retirees own or will own some bonds, it’s worth delving into it.Â

When we peel back the onion today, I hope you realize this question is equivalent to:

- Would you rather buy your eggs one at a time?

- …or by the dozen?

It doesn’t change the egg. It doesn’t change the meals you could make. It doesn’t change the space in your fridge. They’re the same eggs.

So –

Should retirees own individual bonds instead of bond funds, or vice versa?

Maturity = The Root of the Issue

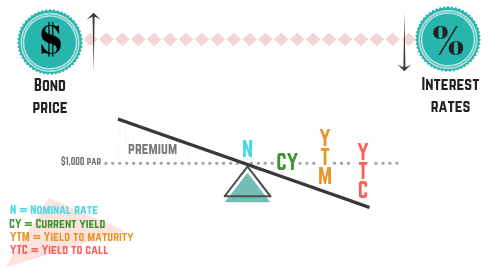

The root of the issue is that individual bonds mature. Eventually, they return their face value back to the owners, plus interest.

If interest rates go up and bond prices fall, the owners tend to think, “Well – I’ll just hold it to maturity and get my full value back.†The bond owners feel like they can ignore the price. It’s borderline imaginary.Â

But bond funds don’t mature. They only return interest. To get your capital back, you’d need to sell shares of the fund – possibly at a loss! The same interest rate hike that the individual bond owners ignored feels much harder to ignore when it’s a bond fund.Â

But What Is a Bond Fund?

But what is a bond fund? What does a bond fund hold? Isn’t it…nothing more than the sum of many individual bonds?Â

If people have convinced themselves to ignore price changes in individual bonds, why can’t we do the same in bond funds?Â

The Maturity Reset

There is one vital difference between individual bonds and bond funds. As far as I’m concerned, this is the ONLY difference that holds water in this conversation.Â

Bond funds (and those who run them) tend to “reset†the funds’ durations regularly. Most individual investors, on the other hand, only do so sporadically.Â

What does that mean, exactly? Â

Take BSV – the Vanguard Short-Term Bond ETF. It holds a slew of 1- to 5-year US Treasury bonds and currently has an average duration of 2.6 years.Â

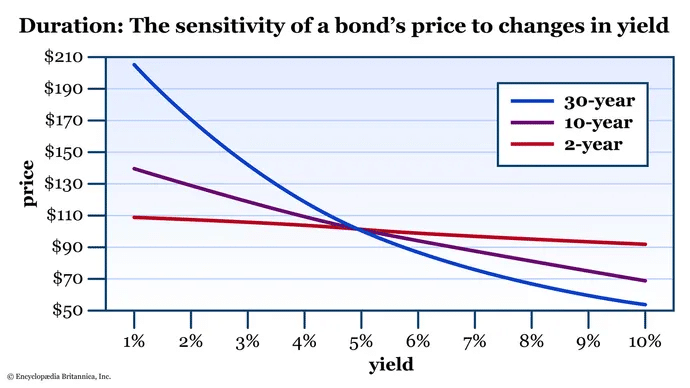

Duration, as a reminder, is a measure of interest rate sensitivity.Â

Every day, the individual bonds in BSV get one day closer to maturity. Every day, the overall duration of BSV ticks downward. And if the fund managers stood by and did nothing, the fund would eventually completely mature and return all its capital to its owners.Â

But BSV has a job, and that job is not to reach maturity. Its job is to maintain a duration in the mid-2.X range. That’s the purpose of this specific tool, and many investors depend on it maintaining its predefined purpose. To accomplish this, the fund managers regularly trim here, trim there, and reinvest fund income into longer-duration bonds to offset the remaining bonds as they shimmy toward maturity.Â

That’s how bond funds like BSV work.

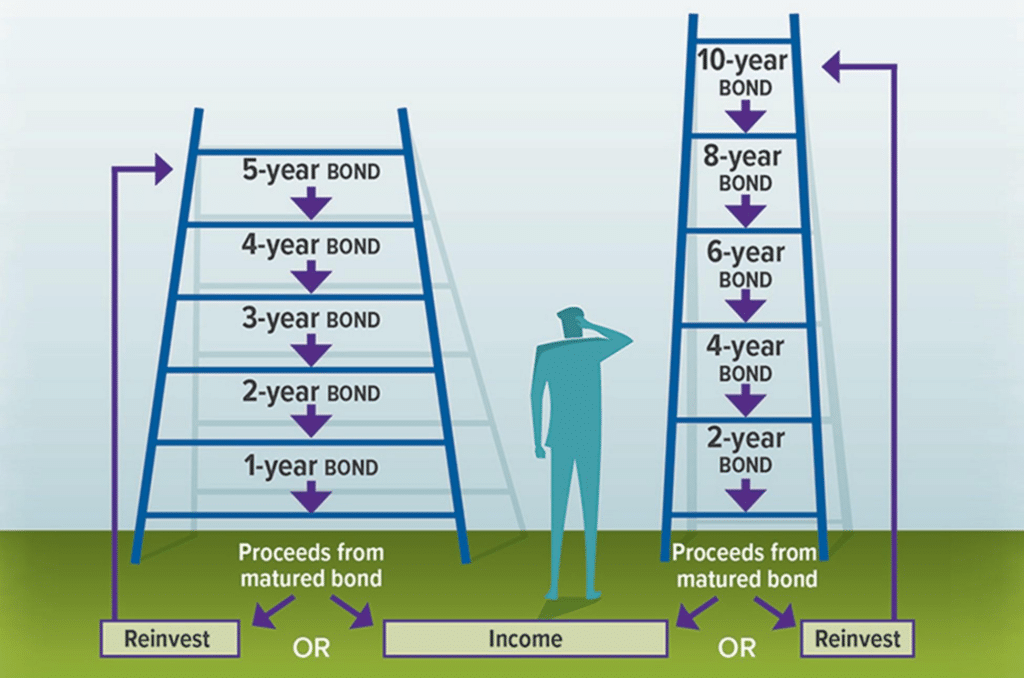

But let’s now compare that to Joe Retiree, aka “Mr. DIY Bond Ladder.â€Â

Joe might have $50,000 in each of 1-, 2-, 3-, 4-, and 5-year Treasury bonds. Every day, Joe’s bond ladder gets one day closer to maturity. Every day, the overall duration of Joe’s bond exposure ticks downward.Â

But unlike the fund managers for BSV, Joe doesn’t care. In fact, this is probably what Joe had in mind. It’s truly a feature, not a bug. Joe wants his 1-year Treasury to mature soon. He wants that capital to fund his retirement. Then he’ll rebalance his portfolio to free up $50,000 to buy a new, shiny 5-year bond. Laddering achieved.

Let’s pause.Â

Do you see what just happened there? Did ya catch it?!

Joe Retiree is doing exactly what the BSV fund manager is doing. He’s resetting his duration. Joe is only doing it once a year, whereas the BSV manager might be doing it once a week.Â

That’s the only difference!  They’re basically the same!

Would You Rather?

Quick aside – would you rather purchase…

- A 10-year bond, price = $1000, yield = 2%

- A 10-year bond, price = $900, yield = 3%Â

Trick question. They lead to the same result. 10 years from now, you’ll have $1200 in hand from either bond.**Â

Price and interest rate are countervailing forces. The price of your bonds might be down, but that’s because the yield has increased in an equal-but-opposite way. And if the price of your bonds rises, the yield decreases. It’s cold, mechanical math.Â

(**Yes – the cashflows will be different and, if we apply a discount rate, the end result might be different. But please accept this simple example for what it is)

But the Fund Price – It’s Still Down!

I know some of you might be saying, “But my bond funds…their prices are still down since 2022!!!â€Â

It’s true.Â

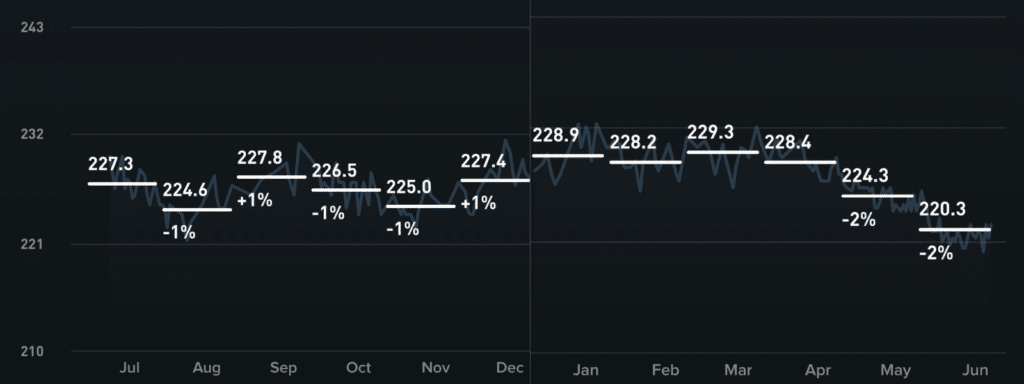

This is a chart for AGG (its duration is ~6 years). It’s still down 15% since 2022. Still hasn’t recovered (though its owners have been receiving an interest stream along the way).

But AGG is a fund. The managers are consistently resetting the duration.Â

If Joe Retiree had built something like a ~12-year bond ladder in 2022; its duration would be equivalent to AGG. And if Joe had done that, where would his bond ladder be now?Â

His longer-duration individual bonds would have taken a beating in 2022, and they’d still be underwater. Joe could assuage himself by saying, “They don’t feel underwater to me. I’ll just wait til they mature in 6, 7, 8 years.â€Â

That’s fine if it makes Joe feel better.Â

But mathematically, Joe’s revolving bond ladder has matched AGG step for step along the way. Joe rebalances his ladder once a year, whereas AGG rebalances much more frequently. That’s the only difference.Â

Other than that…

- The cashflows are the same.Â

- The portfolio values are the same.Â

- The yields are the same.Â

Everything is the same.Â

Bond funds are collections of individual bonds. A retiree’s bond ladder is exactly the same.Â

Aside from any “tracking error†due to rebalancing frequency, we shouldn’t expect any significant differences.Â

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors†has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Khan Academy Blog

Khan Academy Blog  Global Green

Global Green  The Politics Guys

The Politics Guys  Monevator

Monevator  CNBC » World News

CNBC » World News  Radical FIRE

Radical FIRE