Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Tune in on:

Now, here’s today’s article:

Honest Abe Lincoln had a riddle he would tell. He would ask an audience, “How many legs does a dog have if you count its tail as a leg?â€

That’s a strange question, you might think. But, not wanting to make a fool of yourself in front of the President, you might stutter out, “Well…four plus one would give you five legs. Is it five legs, Abe?â€Â

And Abe would scream at you, “Idiot! I fooled you! Don’t you know anything about dogs!?!?â€

And Abe would calmly say, “The fact that you call it a leg doesn’t make it a leg. The answer is four.â€Â

You got ’em, Abe.

He was pointing out the tension (sometimes accidental, sometimes purposeful) between labels, perceptions, etc., vs. the true underlying reality.

Comedian George Carlin was famous for his linguistic bits. Specifically, he spoke and joked about words “that hide truth, that conceal reality, euphemistic language.â€Â

Warning – just a few curse words…

And Charlie Munger, one of my personal favorites, believed that all humans are prone to this behavior.

For example, he once said, “the nature of human psychology is such that you’ll torture reality so that it fits your models.“

When we’re faced with a harsh truth that alters our fundamental beliefs, an innate instinct wants to deny that truth or shoehorn it into our preconceived reality.

Lying with Numbers

In one financial example, Munger was a vocal and sharp critic of “creative accounting.†Too many people lie too often using numbers.Â

Munger would point at a derivatives trade between two large Wall Street firms. Each firm’s accountants then track that trade in their internal accounting books, and each firm’s accountants…show a profit?! How can both profit? This type of behavior is surprisingly common, even though, as Munger would say, “it violates the most elemental principles of common sense.â€Â

Why, though? Why is this happening?Â

Because, in this case, employees at each of those firms have incentives to have their trades appear profitable. Show me the incentives, I’ll show you the outcomes. Â

Can this problem be fixed? Specifically about public accounting, Munger says, “Oh. You’re talking about a problem so deeply rooted in human nature, you won’t live long enough to see it. If it gets 20% fixed in your remaining lifetime, you’ll be a fortunate man.â€Â

Torturing Retirement Numbers

Why am I bringing this up? Who cares about “torturing numbers?â€

Because I think it’s important we avoid this pitfall in our personal financial planning, our portfolio decisions, our retirement planning, etc. It can be all too easy to torture these numbers. Sometimes accidentally. Sometimes to avoid painful realizations. Usually, though, because we simply don’t know any better.

Here are some big examples:

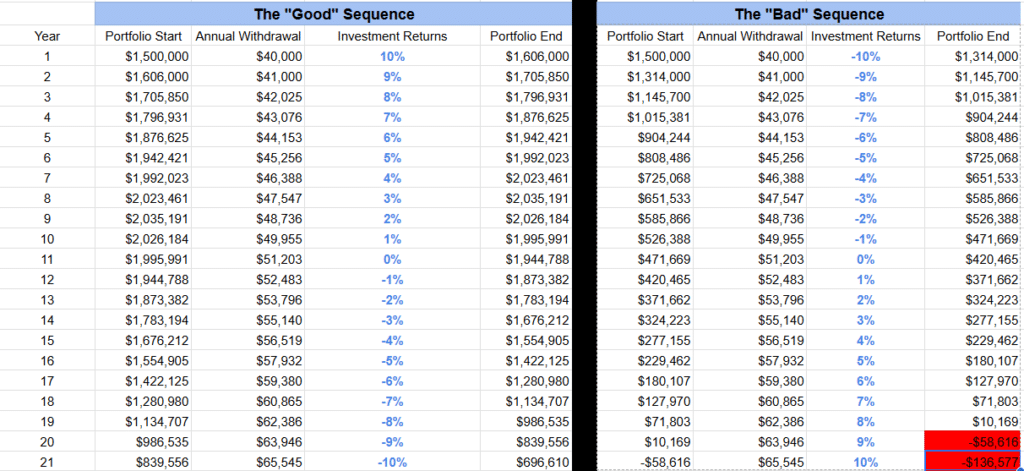

Using “Average Returns†as the Only Model

Unfortunately, your “average returns†in retirement aren’t nearly as important as the specific sequence of returns that you live through.

What will your sequence be? That’s hard to answer. My crystal ball is as foggy as yours.

But simulating various sequences (from rosey to scary) provides far more information than using an average.

Bad Base Assumptions (in either direction!)Â

If you want to use 4% as your go-forward inflation assumption, you’d better have a good reason why.

If you want to use 12% as your average stock market return, you’d better have a reason why.

I caught some flak for saying that I use 8% for stocks (5% once you count inflation)…but I do think I have some good reasons why that’s the case.Â

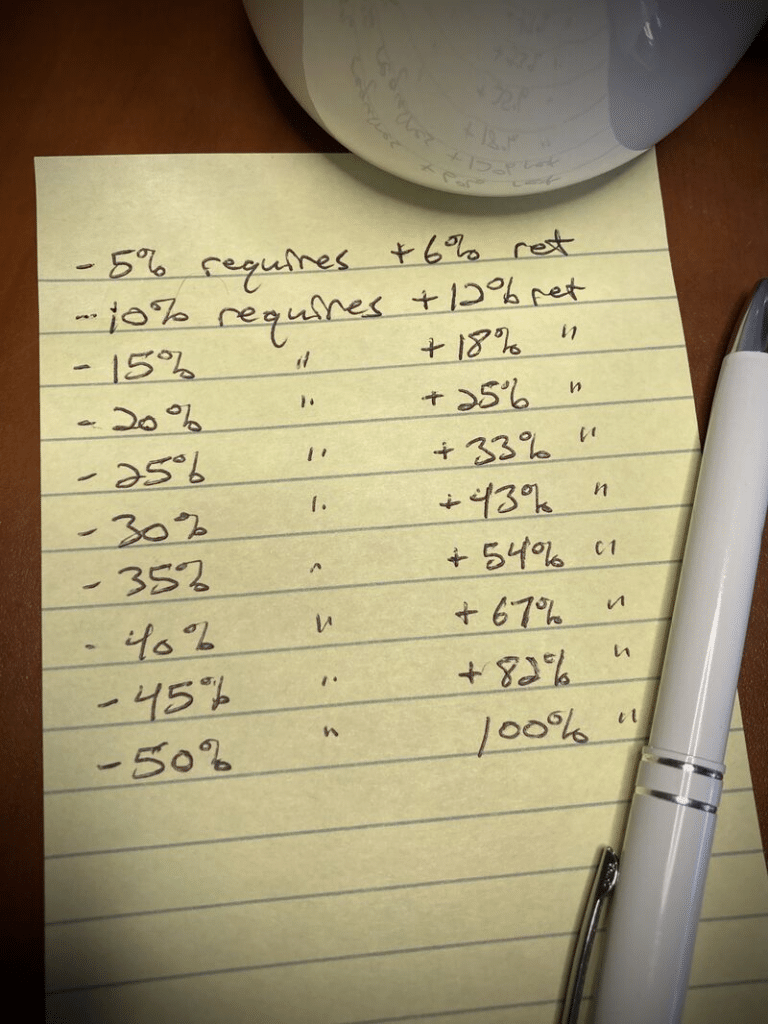

If we use numbers that are unrealistic and unjustifiable – either too optimistic or too pessimistic – we might not be bending reality, but breaking it.

Not Understanding Longevity Data.Â

If you’re planning for retirement, you must understand your longevity data. But retirees make two common mistakes with longevity data.

The first concerns “conditional probabilities.â€Â A simple example – notice the subtle difference between these two statements:

- “The average life expectancy for all men is…â€

- “The average life expectancy for men who have survived to age 60 is…â€

We could re-write the first statement as, “The average life expectancy for all men, including those who die before age 60…â€

…and now the difference in those statements is quite stark. One includes all premature deaths. The other does not. We’d expect those two life expectancy averages to be quite different.

For retirees, only the second statement matters!  You care about your potential longevity, conditional upon the fact that you’ve already made it to your point in life.

Now, the second common mistake with longevity concerns distributions. This graph might look a little wonky, but let me explain it simply:

First, it shows data for men born in 1954 who, as of 2016, had reached age 62. In other words, it’s the “good data†that we just discussed a minute ago, that’s “conditional upon surviving to current age.â€

The horizontal / x-axis shows future age. That’s pretty simple.

The green line corresponds to the left vertical / y-axis. It says, “For this group of 62-year-old men, what are the odds you’re still alive at this specific age?â€

Age 70? About 90%.

Age 80? About 65%.

Age 100? About 5%.

The red bars correspond to the right vertical / y-axis. These red bars say, “For this group of 62-year-old men, what are the odds you die at this specific age?â€

Age 70? About ~1.8% of the group will die at 70.

Age 80? About ~3.0% of the group will die at age 80.

Age 100? About ~1.0% of the group will die at age 100.

For this cohort, there’s a ~1/3 chance you’re dead by 80.

There’s a ~1/3 chance you live past 90.

And the last 1/3, therefore, involves death between 80 and 90.Â

Longevity isn’t one number. It’s a spectrum of numbers. That makes it a real challenge to plan around. But, you cannot and should not torture longevity into one single numnber.

This article could probably go on and on, but I don’t want to torture the idea much further. Numbers can easily fool us if we’re not careful.

“It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.â€

Charlie Munger

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors†has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!